First Quarter Effect in Stocks

Earlier this

year, we researched a so-called January Effect on the stock market. In that

article, we found evidence that there is a stronger correlation between

positive market returns in January and positive 12 month returns, than when

returns are negative in January preluding negative 12 month returns.

In a recent article on seekingalpha.com, Tiger Technologies ventured to

find whether there is a relationship between first quarter returns (returns in

the first three months of a year) and full year returns, or whether there is a

First Quarter Effect. The company’s conclusions confirmed such a relationship,

and observed that it is quite similar to the January Effect.

Tiger Technologies took the quarterly and annual returns of the S&P

500 index over the period 1952-2013 and ran a correlation analysis of first

quarter returns and the returns for the rest of the year. They found that the

first quarter had the highest correlation (15%) among all quarters to the

performance of the sum of the remaining three quarters (from -5% to 13%).

They looked deeper and studied the direction and size of those returns

and found that 39% of the studied years (23 years) had negative first quarter

returns. Out of those 23 years, only 10 years, or 43%, saw full year results

negative as well. This resembles the evidence about the January Effect: a negative

start of the year does not necessarily indicate that the rest of the year will

also be negative.

As to positive first quarters, first quarter returns were in the black

in 36 out of 59 years. In 33 years (92% of 36), the full year stock market return

was also positive. In other words, a positive first quarter has 92% of the time

led to a positive full year return.

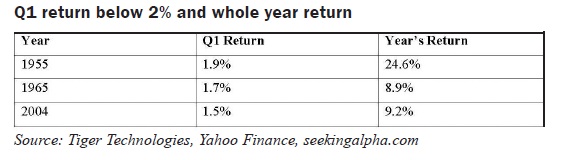

Tiger Technologies used this analysis to forecast the S&P 500 index

result for 2014. In Q1/2014, the S&P 500 index grew by 1.7%. The company’s

analysis showed that a positive first quarter has led to a positive year 92% of

the time and a first quarter growth of 1%-2% has led to a positive year 100% of

the time (although there were only three such years between 1952-2013, see the

table).

This sounds quite good in terms of S&P 500 chances to have a

positive return in 2014. At the same time, we would like to warn those who may

want to quantify what the S&P 500 return would be for the whole year 2014

based on this analysis. The average return for S&P 500 in those three years

was 14.2%. However this number cannot be used to gauge this year’s performance

because, in particular, the data, which was used for this study, is limited.

And we have to cite our usual caveat in this kind of situations: past

performance is no guarantee of future returns.

Michael Zienchuk, MBA, CIM

Investment Advisor, Credential Securities

Inc.

Manager, Wealth Strategies Group,

Ukrainian Credit Union Limited

416-763-5575 x204 mzienchuk@ukrainiancu.com

www.ukrainiancu.com

Mutual funds and other securities are offered through Credential

Securities Inc. Commissions, trailing commissions, management fees and expenses

all may be associated with mutual fund investments. Please read the prospectus

before investing. Unless otherwise stated, mutual funds and other securities

are not insured nor guaranteed, their values change frequently, and past

performance may not be repeated. The information contained in this article was

obtained from sources believed to be reliable; however, we cannot guarantee

that it is accurate or complete. This article is provided as a general source

of information and should not be considered personal investment advice or

solicitation to buy or sell any mutual funds and other securities. The views

expressed are those of the author and not necessarily those of Credential

Securities Inc. Credential Securities Inc. is a Member of the Canadian Investor

Protection Fund.